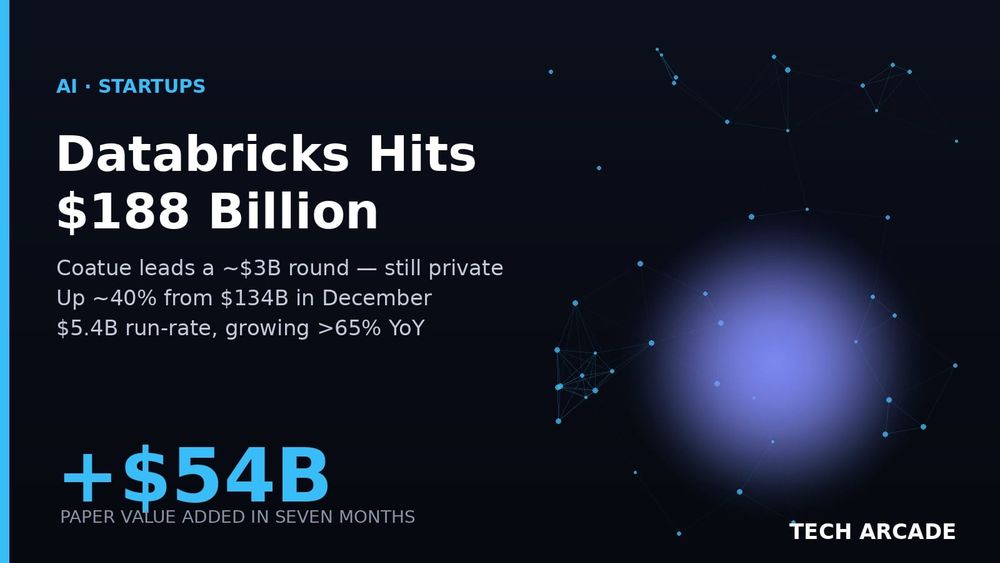

Here's a number to sit with: $188 billion. That's the price tag on Databricks after its newest funding round — the one it announced this week, led by existing backer Coatue (Databricks, Bloomberg).

Seven months ago, in December, the same company closed a round at $134 billion (Databricks). So in the time it takes most companies to redesign a logo, Databricks tacked on roughly $54 billion in paper value — a ~40% jump (AI Weekly). The new money is a reported $3 billion (Yahoo Finance).

And it did all of this while still stubbornly, conspicuously private. No IPO. No ticker. No opening-bell confetti.

The thesis: the most valuable AI infrastructure company you can't buy a share of just repriced itself 40% higher in half a year — and the public markets are watching from the cheap seats.

🧠 Why This Matters

Valuations in AI have gotten so large they've stopped feeling real. A 40% bump sounds like rounding error next to trillion-dollar headlines. But $54 billion of fresh value is not abstract — it's larger than the entire market cap of many companies in the S&P 500.

What makes Databricks different from the pure-model crowd is that it isn't selling intelligence by the token. It sells the plumbing — the data lakehouse where enterprises store, govern, and actually put their information to work. When every company on earth wants to build AI on top of their own data, Databricks is the floor they're standing on. That's a boring, beautiful, deeply sticky place to be.

CEO Ali Ghodsi framed the moment with a line that's already doing laps on tech Twitter:

"Enterprises are moving from tokenmaxxing to valuemaxxing. They don't want to burn expensive tokens on the smartest model for every task — they want the best outcome per dollar." — Ali Ghodsi, Co-founder & CEO, Databricks (AI Weekly)

Translation: the gold-rush phase of "spend anything, the model is magic" is cooling. The next phase rewards whoever makes AI pay off. Databricks is betting the house that it owns that layer.

📊 Deep Dive

Strip away the vibes and the fundamentals are genuinely loud. Back in February, Databricks said it had crossed a $5.4 billion revenue run-rate, growing more than 65% year over year, with an AI-specific run-rate of $1.4 billion (Databricks). This is not a pre-revenue moonshot. It's a company selling a lot of software, fast.

Here's the trajectory, laid out:

- December 2025: Series L closes at a $134B valuation, raising more than $4B, on a $4.8B run-rate growing >55% YoY (Databricks).

- February 2026: run-rate ticks to $5.4B, growth accelerates to >65%, AI run-rate hits $1.4B (Databricks).

- Secondary markets (mid-2026): shares reportedly changing hands in the $165–175B range before this round (AI Weekly).

- July 2026: new round pins it at $188B — leapfrogging that secondary-market estimate.

Notice the thing most companies would kill for: growth speeding up as revenue gets bigger. Going from 55% to 65% YoY on a multibillion-dollar base is the kind of curve that makes investors sign term sheets before breakfast.

The new capital is earmarked for three products with very Databricks names: Unity AI Gateway (governance across every model you use), Genie (let any employee just talk to their data), and Lakebase (a serverless Postgres built for AI agents) (Databricks).

⚠️ The Catch

Deep breath, because a few caveats deserve airtime.

First, run-rate is not revenue. A run-rate annualizes a recent period — it's a snapshot multiplied out, not a closed fiscal year. It's a legitimate metric, but it flatters fast-growers by design.

Second, at $188B on a ~$5.4B run-rate, you're paying somewhere north of 30x revenue. That's a price that assumes the growth doesn't just continue — it compounds. Any stumble and the multiple looks brutal.

Third, private valuations are negotiated, not discovered. A single lead investor and a term sheet set this number. The public market — where thousands of sellers vote every second — hasn't gotten its say. As Databricks itself notes, it still competes head-on with a very public Snowflake, whose stock reprices daily whether management likes it or not.

🎯 What Happens Next

The round is a term sheet expected to close over the summer, not a done deal already wired (Yahoo Finance). Watch for the final figure — reported at ~$3B — and whether the investor list grows.

The bigger question is the one nobody at Databricks will answer directly: when's the IPO? Every raise at this scale buys the company more runway to stay private and more pressure to eventually go public. Employees holding options and early VCs eventually want liquidity that isn't just a secondary-market trickle.

And keep an eye on those three products. If Genie and Lakebase convert into their own run-rate lines the way the core AI business did — from $0 to $1.4B — the next repricing won't need seven months.

🧩 Bigger Picture

Zoom out and Databricks is the clearest sign yet that the AI money has split into two leagues. Up top, the frontier-model labs — Anthropic reportedly nearing a $1 trillion valuation, overtaking OpenAI (CNBC) — burn staggering sums chasing raw intelligence. One rung down sits the picks-and-shovels tier: the data, governance, and deployment layer where Databricks lives, quietly charging everyone who wants to actually use that intelligence.

History says the shovel-sellers often outlast the prospectors. Ghodsi's "valuemaxxing" pivot is a bet that the market is about to reward exactly that discipline. A $54 billion raise in seven months suggests a lot of very rich people agree.

The public markets keep asking Databricks when it's finally going to show up. At $188 billion, Databricks keeps answering the same way: it doesn't need to.

Sources

- Databricks — Raising a Strategic Round of Funding at a $188 Billion Valuation

- Bloomberg — Coatue Leads Databricks Funding Round at $188 Billion Valuation

- Yahoo Finance — Databricks Valued at $188 Billion in Coatue-Led Round

- AI Weekly — Coatue Leads $3B Investment in Databricks at $188B Valuation, 40% Above December Mark

- Databricks — Grows >65% YoY, Surpasses $5.4 Billion Revenue Run-Rate

- Databricks — Surpasses $4.8B Revenue Run-Rate, Raising >$4B Series L at $134B Valuation

- CNBC — Anthropic Tops OpenAI as Most Valuable AI Startup, Nears $1 Trillion Valuation